In the “What market failure” we will look at the various claims that the free market failed, and show that the principles of the free market did not fail, but where coercively distorted by government intervention.

Claim: Due to de-regulation banks decreased their lending standards which lead to giving people mortgages that they couldn’t pay. Banks cannot be trusted to make wise decisions on their own, the free market has failed, thus it must be regulated.

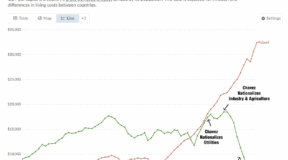

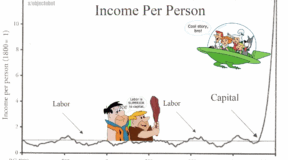

This of-course is not the case. Bank’s incentive to give loans is the profit motive. Giving loans to people who cannot pay them back does not lead to profit but to loss. Banks have been steadily making money from home loans for over 100 years. The banks lowered their lending standards because the government applied sticks(punishment) and carrots (rewards) to change their behavior. The stick in this case was the (CRA), Community reinvestment act, and the carrot was (GSE), government sponsored enterprises, the largest of which are Fannie Mae and Freddie Mac. The CRA is a law that was passed by the government that forced banks to make high-risk loans they would not have otherwise made and that people cannot repay . Failure to comply meant fines and difficulty in getting approval for mergers and branch expansion. While the stick was being applied at the same time the government dangled a carrot. Fannie Mae and Freddie Mac—Government-sponsored enterprises (GSEs), created a credit scoring formula with a very low qualifying score. They tell banks and other lending institutions, “If you make home loans to anyone who meets our low qualifying score, we will buy the loans from you at a profit to you.” The lenders play along and make the bad loans. The Fannie Mae plays along too and buy the bad loans from the lenders. The GSE’s create a portfolio of about $6 trillion (half the mortgage market) in this manner. Remember Fannie Mae, even though it is traded publicly on the NYSE is government sponsored, as in its debt has an implicit guarantee by the federal government. Without their debt being implicitly guaranteed by the federal government, Fannie and Freddie would not have been able to have consistently fund themselves, which means they would never been able to take on so many loans. With less bad loans begin bought by Fannie, there would have been less demand for the product. With less demand, there would have been less product originated and fewer credit problems to deal with today. When questions began to arise about government policy that intimidated lenders into making high-risk loans, we received congressional assurances. At hearings investigating the solvency of Fannie Mae and Freddie Mac, Rep. Barney Frank said, ”The more people exaggerate these problems, the more pressure there is on these companies, the less we will see in terms of affordable housing.”

1 Comment

What market failure? Final Part. Lets Review. – objectobot.com

(May 30, 2024 - 8:47 pm)[…] government stick, fines, and difficulty in getting approval for mergers and branch expansion. (See Part5). At the same time Fannie Mae, a government-sponsored agency, with its debt being implicitly […]